Revenue-Based Financing: A Complete Guide

Revenue-based financing (RBF) has emerged as a powerful alternative to traditional funding methods for businesses, particularly startups and small-to-medium-sized enterprises (SMEs). Unlike loans that demand repayment regardless of performance, RBF ties repayments directly to a company's revenue, offering a flexible and less risky approach to securing capital. This comprehensive guide will delve into the intricacies of RBF, exploring its benefits, drawbacks, and how to determine if it's the right choice for your business.

What is Revenue-Based Financing?

Revenue-based financing is a type of alternative funding where investors provide capital in exchange for a percentage of future revenue. The repayment schedule is directly tied to the company's revenue stream, making it a low-risk option for both the lender and the borrower. This contrasts sharply with traditional loans, which demand fixed repayments regardless of the business's financial health. There's usually no personal guarantee required, reducing the personal financial burden on the business owner.

How Does Revenue-Based Financing Work?

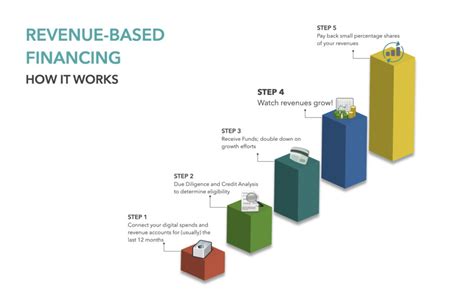

The process typically involves:

- Application: Businesses apply to an RBF provider, outlining their financial projections and business model.

- Due Diligence: The provider assesses the business's viability and revenue potential.

- Funding: If approved, the provider provides a lump sum of capital.

- Repayment: The business repays the investment, plus a pre-agreed percentage of revenue, over a predetermined period. The repayment percentage is typically a fixed amount, but can sometimes be tiered.

- No Equity Dilution: Unlike venture capital or angel investors, RBF providers typically don't acquire equity in the company.

Key Differences from Traditional Loans:

- Repayment Structure: RBF repayments are revenue-dependent, while loans demand fixed payments.

- Risk Allocation: The risk is shared between the investor and the business.

- Equity Ownership: RBF typically doesn't involve equity dilution.

- Flexibility: RBF offers more flexibility and better suits businesses with fluctuating revenue streams.

Advantages of Revenue-Based Financing

- Reduced Risk: Repayments are tied to revenue, making it easier for businesses to manage cash flow during lean periods.

- No Equity Dilution: Businesses maintain full ownership and control.

- Faster Funding: The application and approval process is often quicker than traditional loan applications.

- Flexibility: RBF offers a flexible repayment structure, tailored to the business's specific circumstances.

- Simple Agreement: The terms are often simpler and easier to understand than traditional loan agreements.

Disadvantages of Revenue-Based Financing

- Higher Cost of Capital: The percentage of revenue paid to the investor can be higher than the interest rate on a traditional loan.

- Limited Funding Amounts: RBF providers usually offer smaller funding amounts compared to traditional loans or venture capital.

- Revenue Dependency: Repayment relies entirely on revenue generation; a downturn in revenue can severely impact repayment.

- Potential for High Repayment Amounts: If the business experiences rapid revenue growth, the total amount repaid can be significantly higher than initially anticipated.

Is Revenue-Based Financing Right for Your Business?

RBF can be a beneficial option for businesses that:

- Have predictable revenue streams: Consistent revenue is crucial for managing repayments.

- Need quick access to capital: The process is often faster than traditional loan applications.

- Want to avoid equity dilution: Maintaining full ownership is a major advantage.

- Are experiencing rapid growth: The ability to scale operations with RBF funding can be significant.

However, it may not be suitable for businesses that:

- Have unpredictable revenue streams: Fluctuations in revenue can make repayments challenging.

- Require large funding amounts: RBF providers usually offer smaller investment amounts.

- Are concerned about high repayment amounts based on revenue growth: Careful consideration of potential total repayment is crucial.

Finding a Revenue-Based Financing Provider

Researching different RBF providers is essential. Compare their terms, fees, and repayment structures to find the best fit for your business. It's always advisable to seek professional financial advice before committing to any funding option.

In conclusion, revenue-based financing presents a viable alternative to traditional funding, particularly for businesses with stable revenue streams and a desire to retain ownership. By carefully weighing the advantages and disadvantages and conducting thorough research, businesses can determine if RBF is the right solution to fuel their growth.